pyensmallen

pyensmallen provides Python bindings for the ensmallen optimization library, with a focus on econometrics and supervised learning workflows.

Install

Base install:

uv pip install pyensmallenDevelopment install with all test and notebook dependencies:

uv pip install --python .venv/bin/python ".[full]"Editable install in this repository:

uv pip install --python .venv/bin/python meson meson-python ninja pybind11

uv pip install --python .venv/bin/python --no-build-isolation -e ".[full]"What is included

- Optimizers:

L_BFGS,FrankWolfe,SimplexFrankWolfe, and Adam variants - Objective helpers: linear, logistic, and Poisson losses

- Estimator classes:

LinearRegression,LogisticRegression,PoissonRegression - Inference: classical and robust sandwich standard errors for unregularized OLS and QMLE-style logit and Poisson

- GMM support with JAX autodiff

Documentation map

- Optimizers: low-level optimizer classes and when to use them

- Benchmarks: runtime and convergence comparisons against SciPy and statsmodels

- Estimators: supervised estimators, fitted attributes, and inference

- Notebooks: examples and benchmark notebooks in this repository

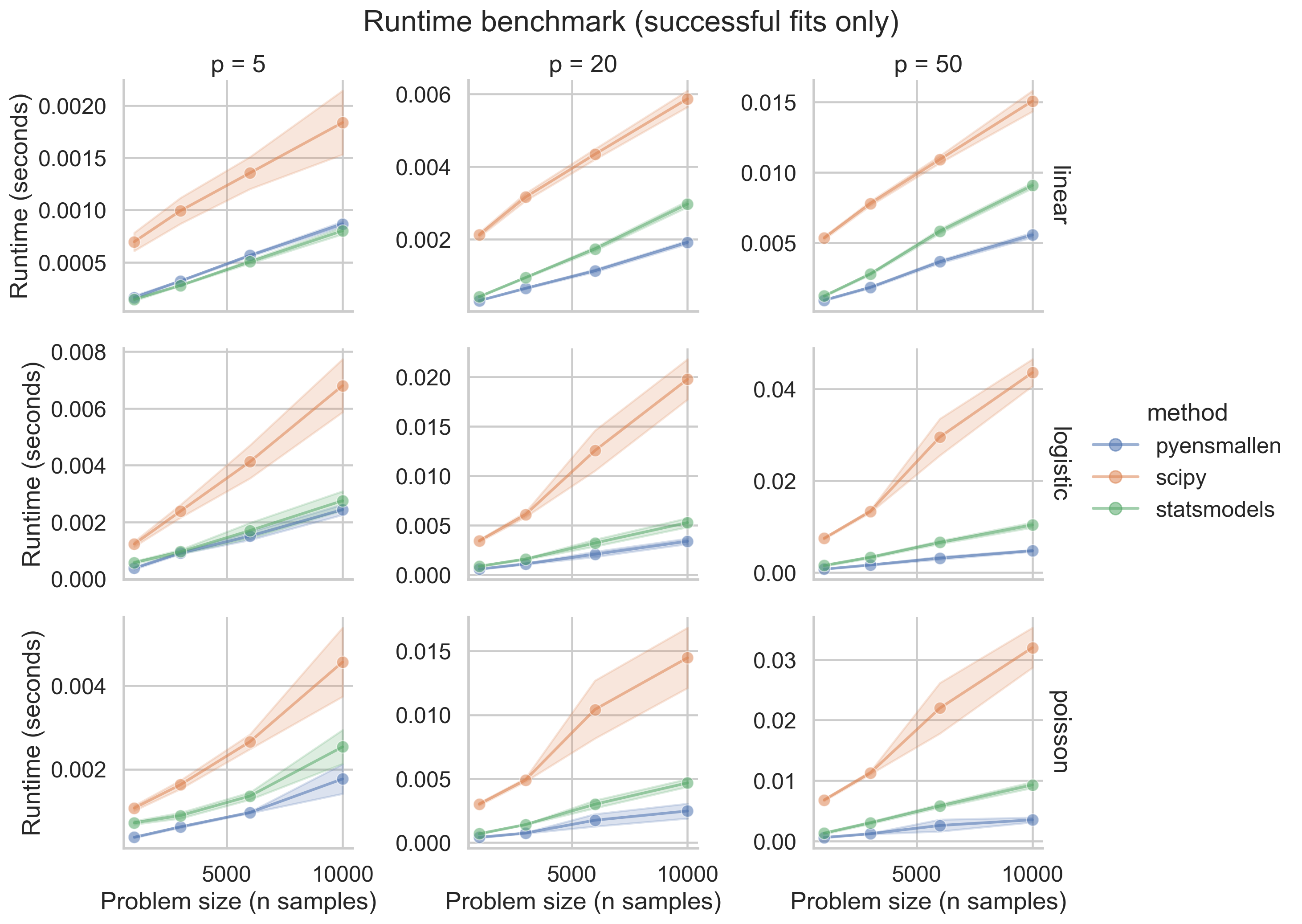

Runtime benchmark snapshot

pyensmallenremains fastest in most medium/large configurations, with widening gaps at largern.- The practical implication is cheaper repeated estimation loops: bootstrap inference, model sweeps, and sensitivity analysis become much more tractable.

- SciPy generally tracks second, while statsmodels is often slower at scale; this compounds heavily in resampling workflows.

Notes

- The

fullextra installs Python packages required to run tests and notebooks. - Quarto itself is an external CLI. Render this site with

scripts/render_docs.sh.